Distilled spirits continue to lead American alcohol sales. With 42.4 percent of market share, spirit sales slightly outpaced beer sales for the fourth straight year. The recent growth in market share, an increase of more than 13 percent since 2000, has been driven in large part by newer products, like ready-to-drink cocktails and hard seltzers.

Innovative products have blurred the lines of the categorical tax system that defines taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. rates based on alcohol type. The spirited competition throughout the alcohol industry and the challenges presented when new products enter the market under the categorical system have spurred calls for reform.

Generally, distilled spirits suffer the stiffest tax rates of all alcoholic beverages. Spirits have a higher alcohol content than wine or beer, but spirits are also taxed at a higher rate per alcohol content than other alcohol types. A standard drink of spirits (a one-ounce shot of 40 percent alcohol) bears a greater tax burden than an identical standard drink of beer (12 ounces of 4.8 percent alcohol), despite both containing 0.4 ounces of alcohol.

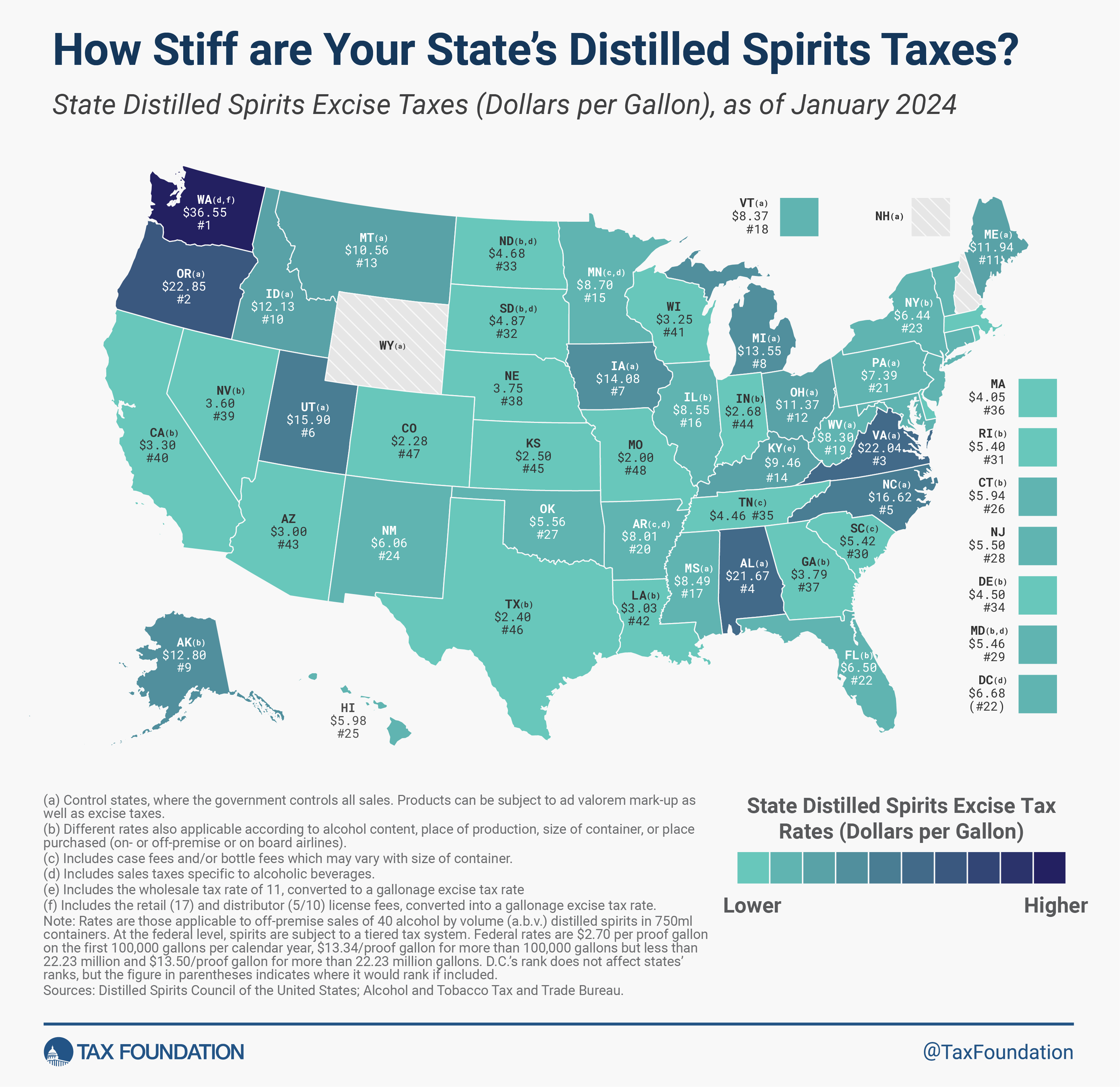

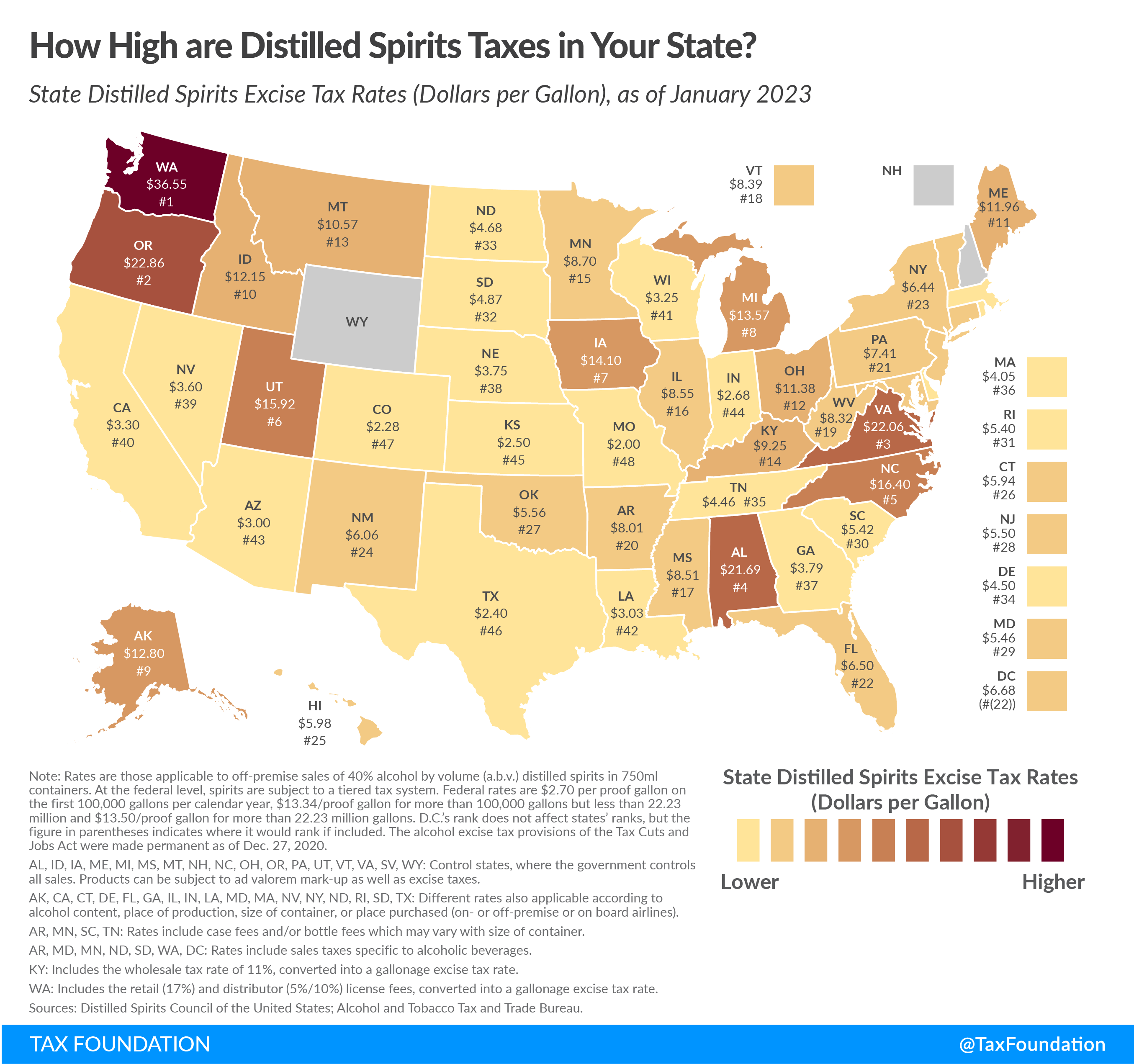

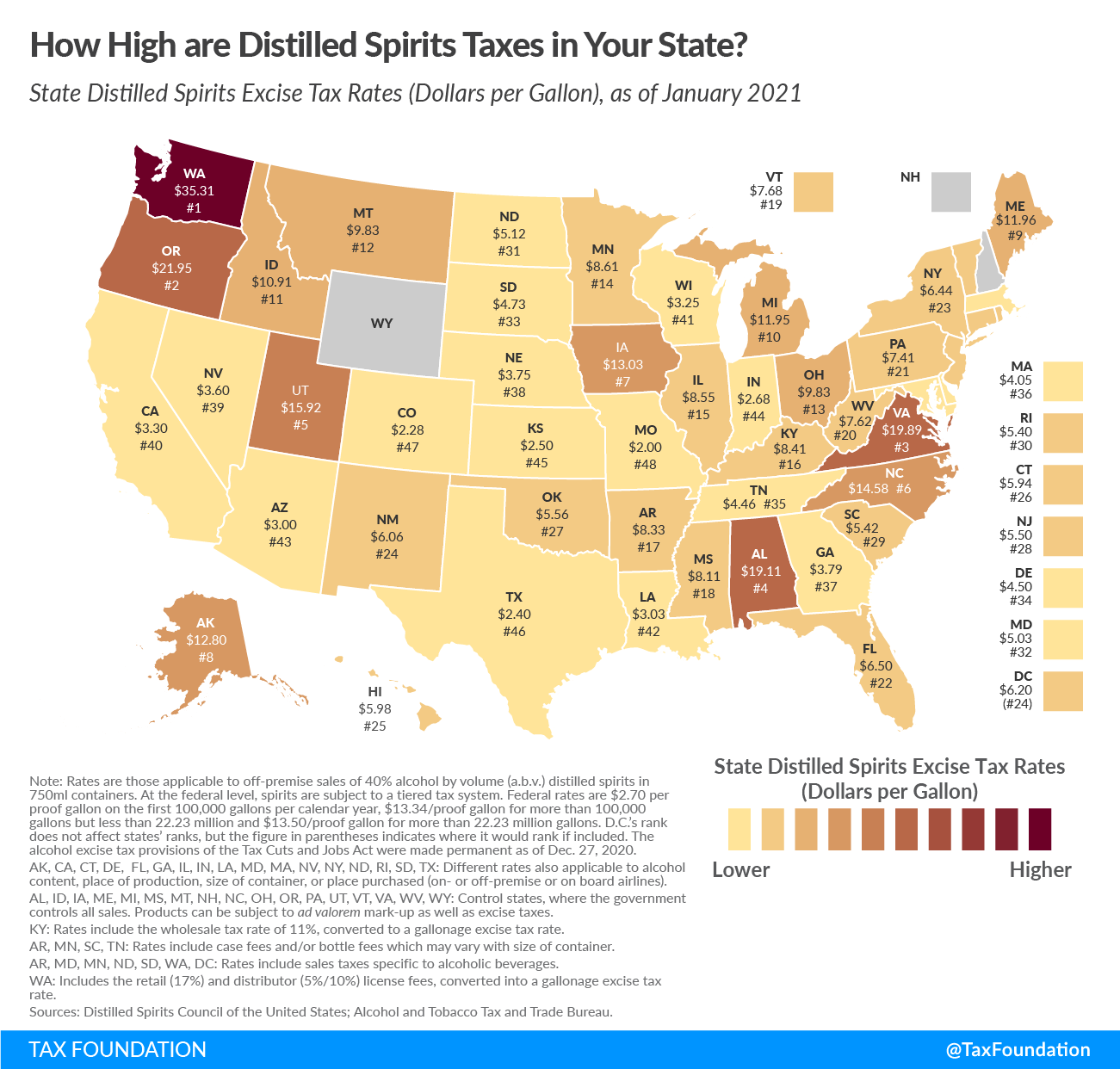

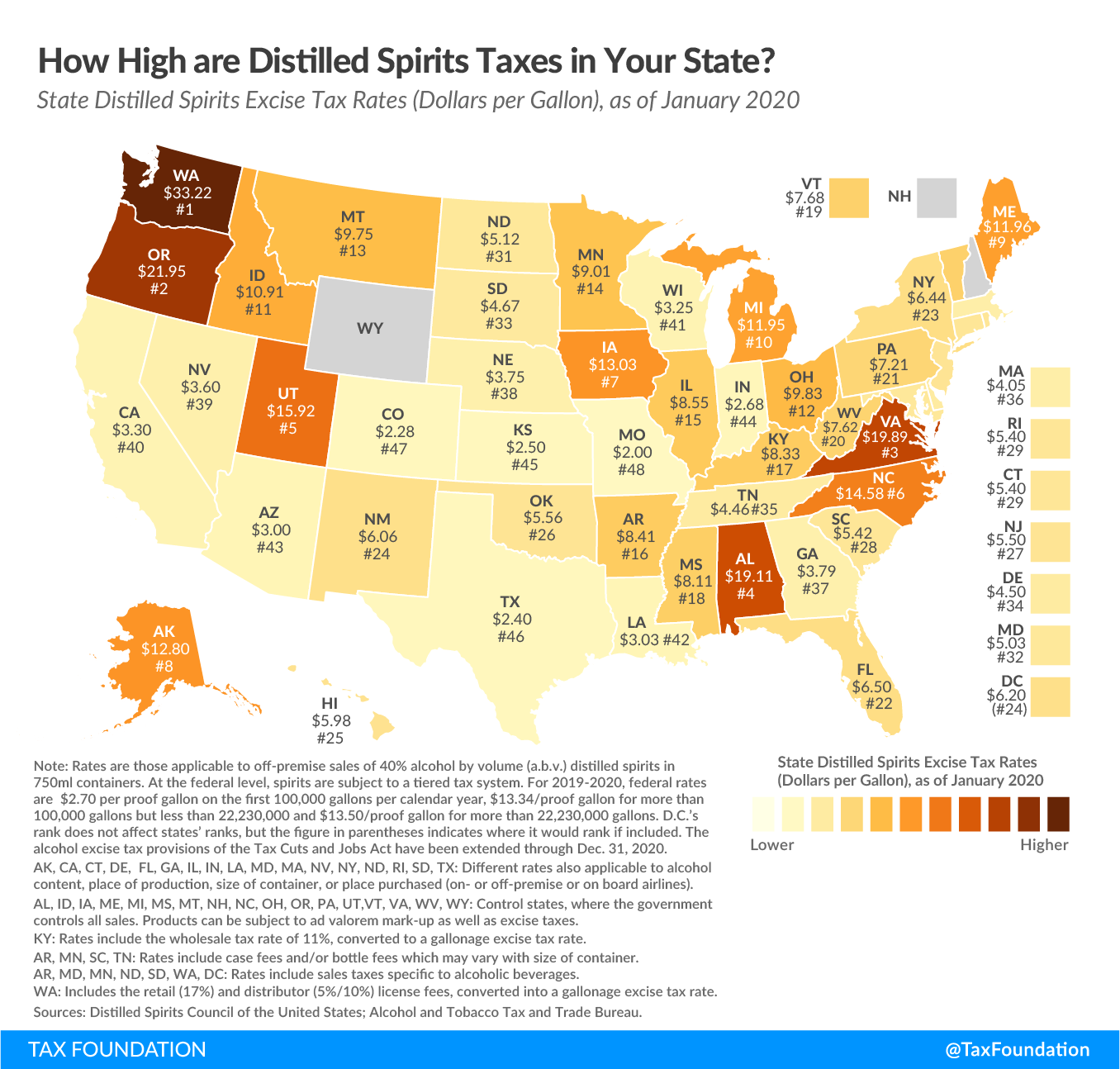

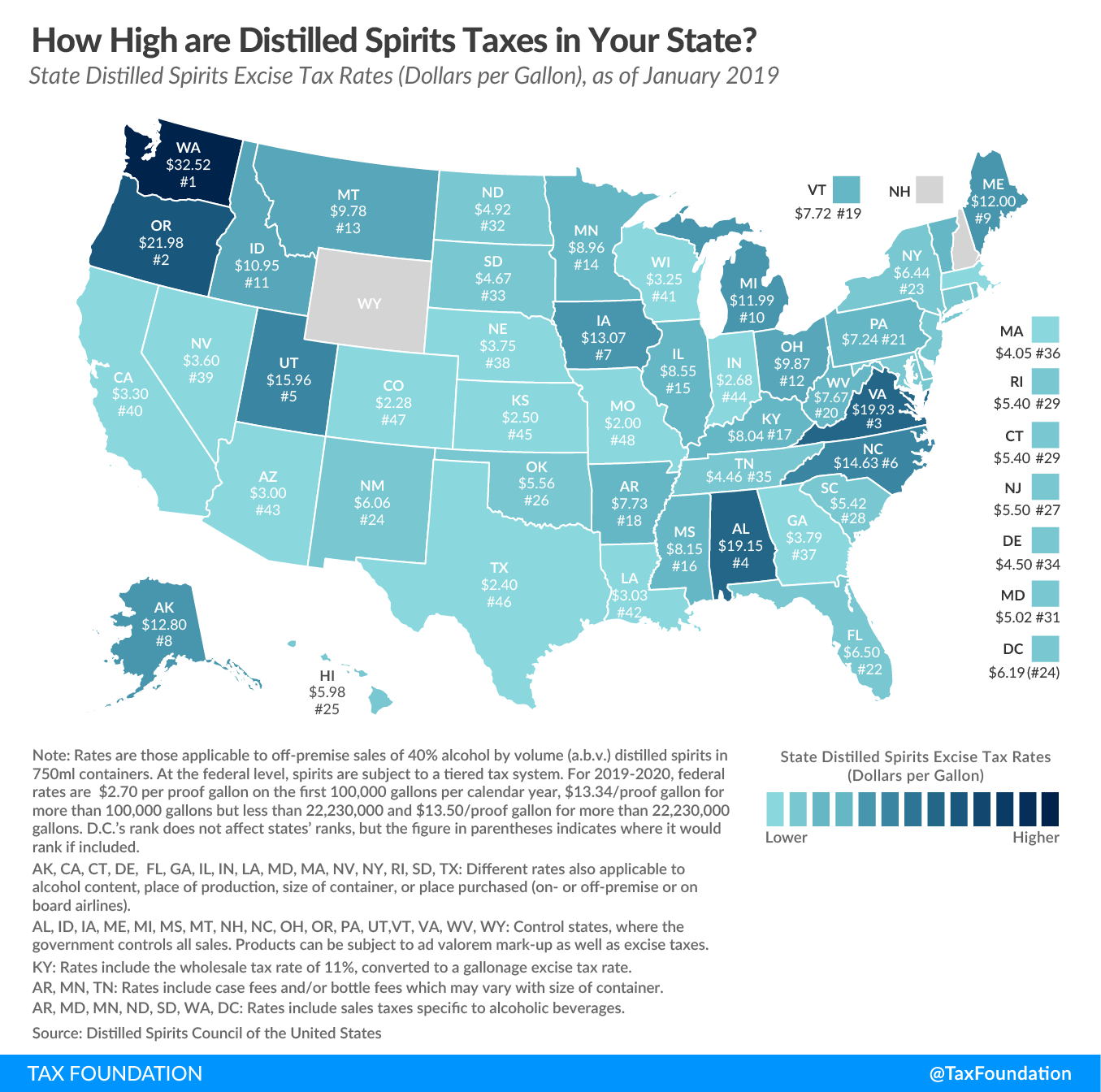

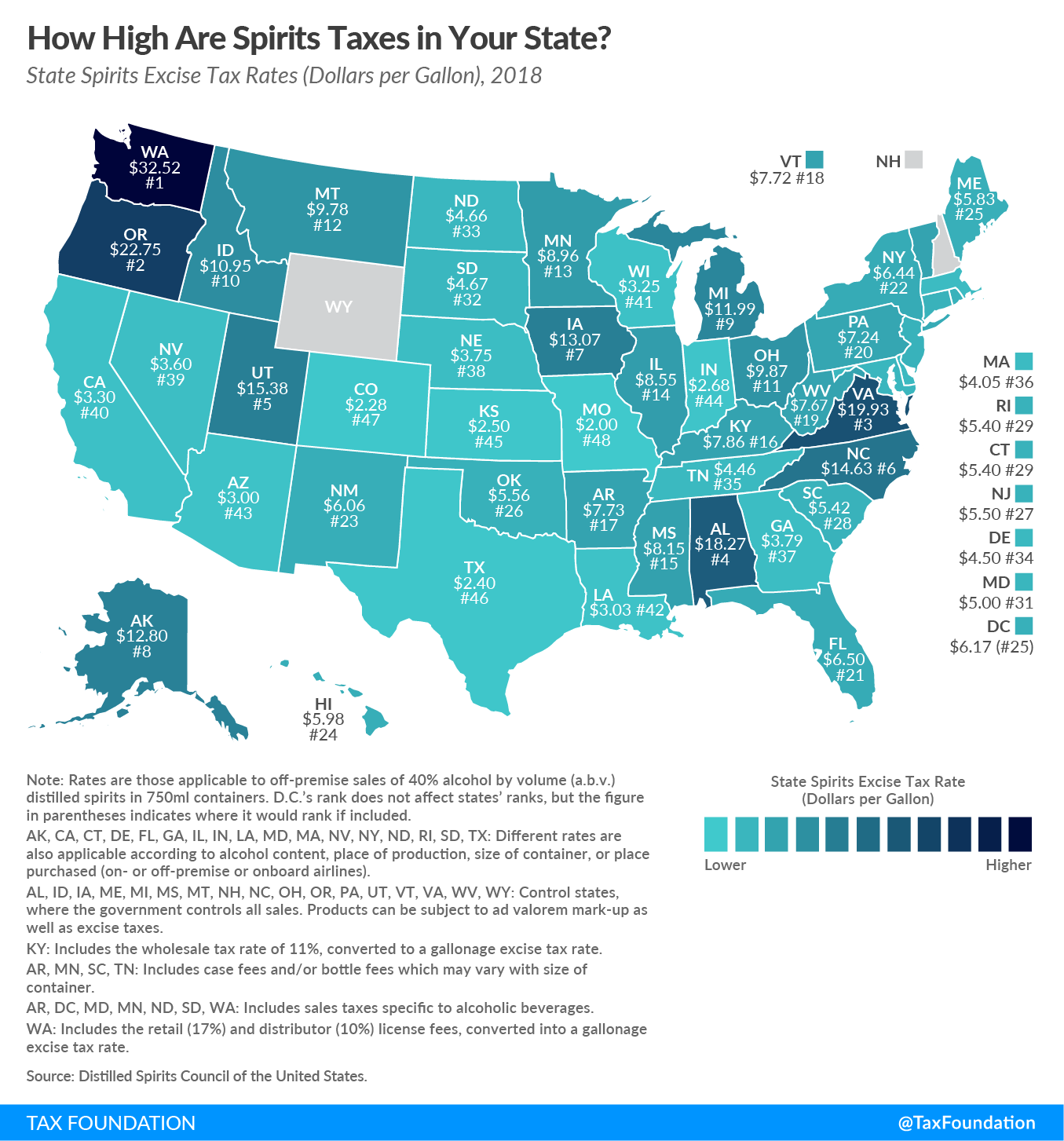

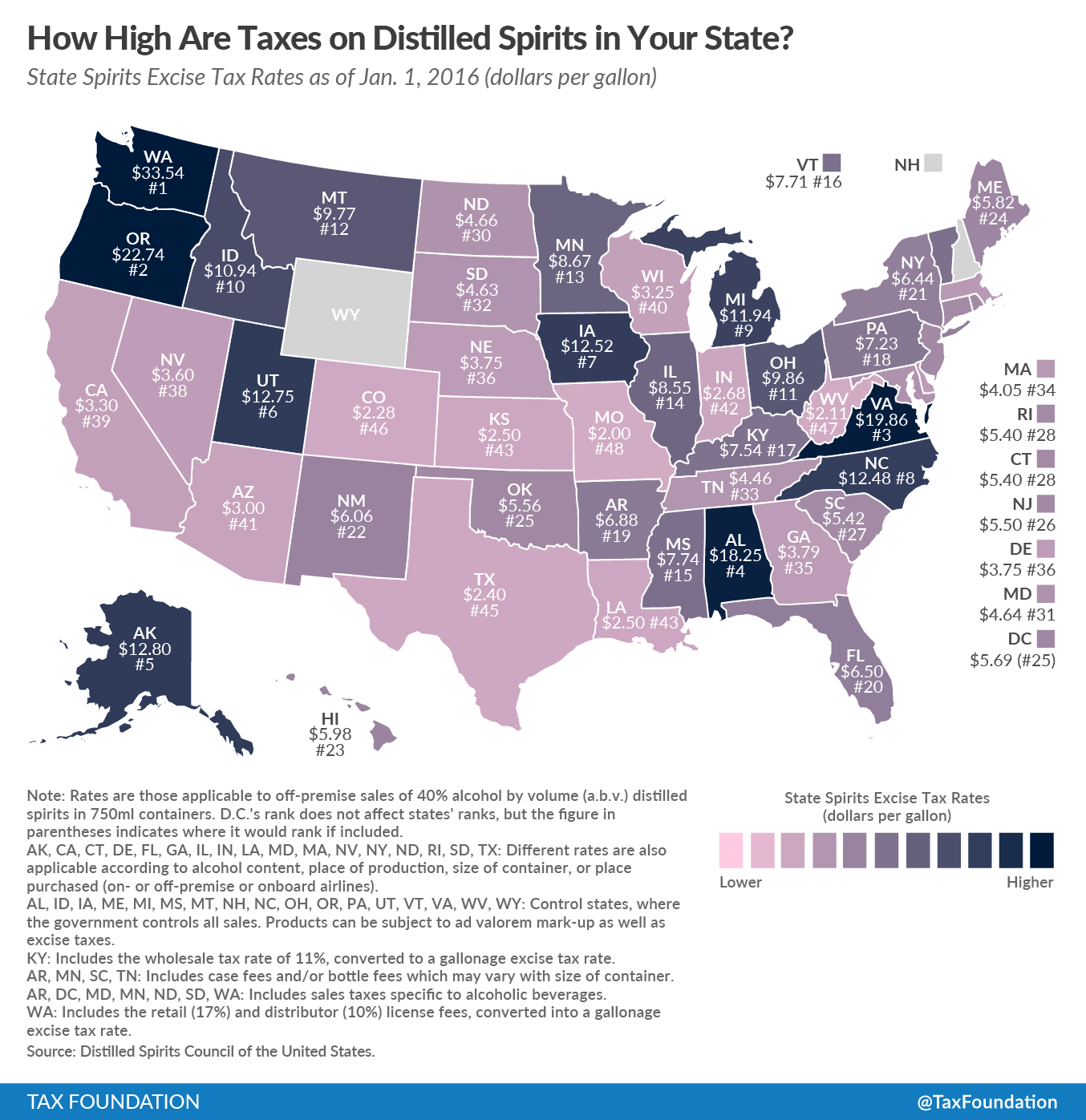

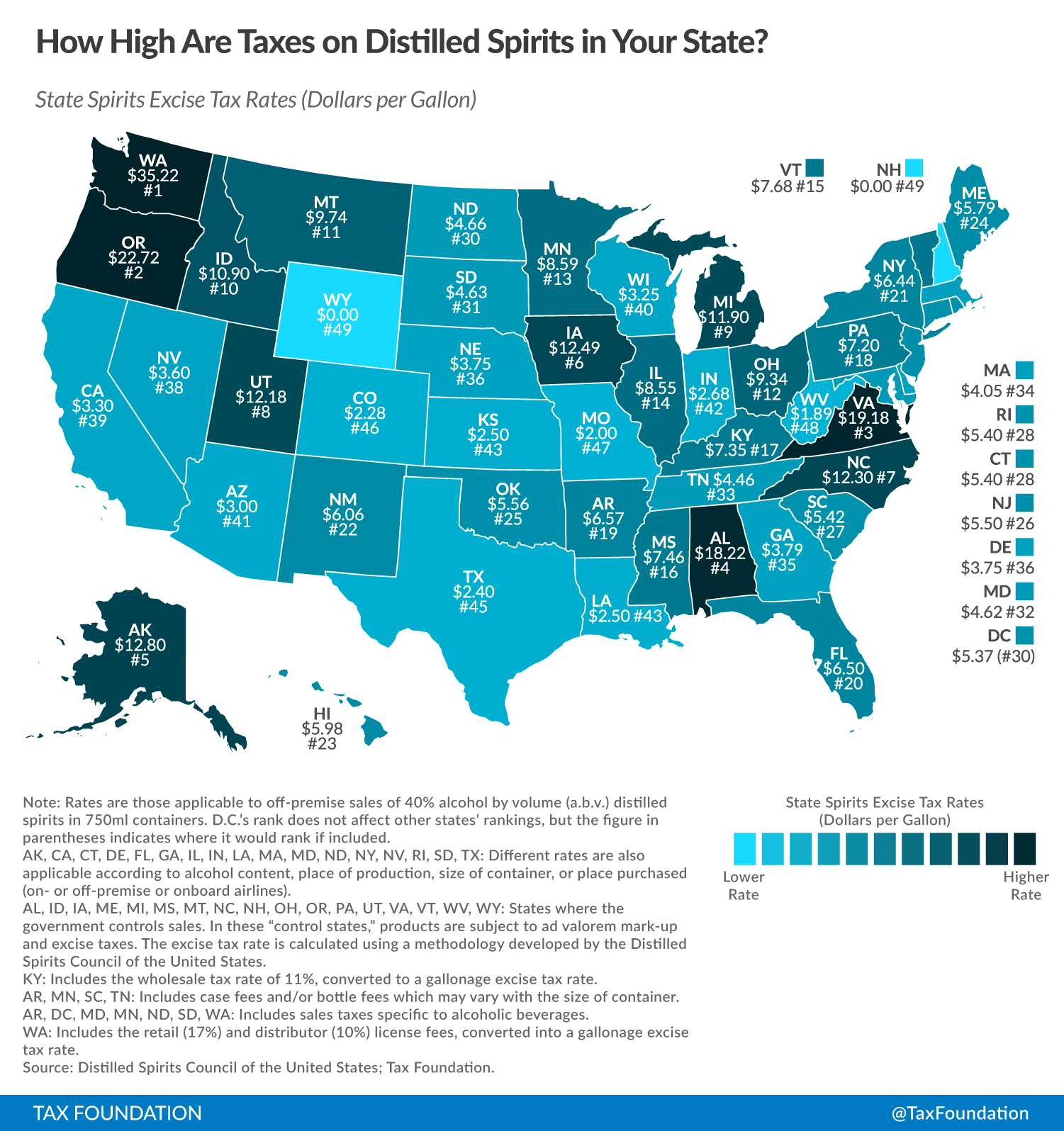

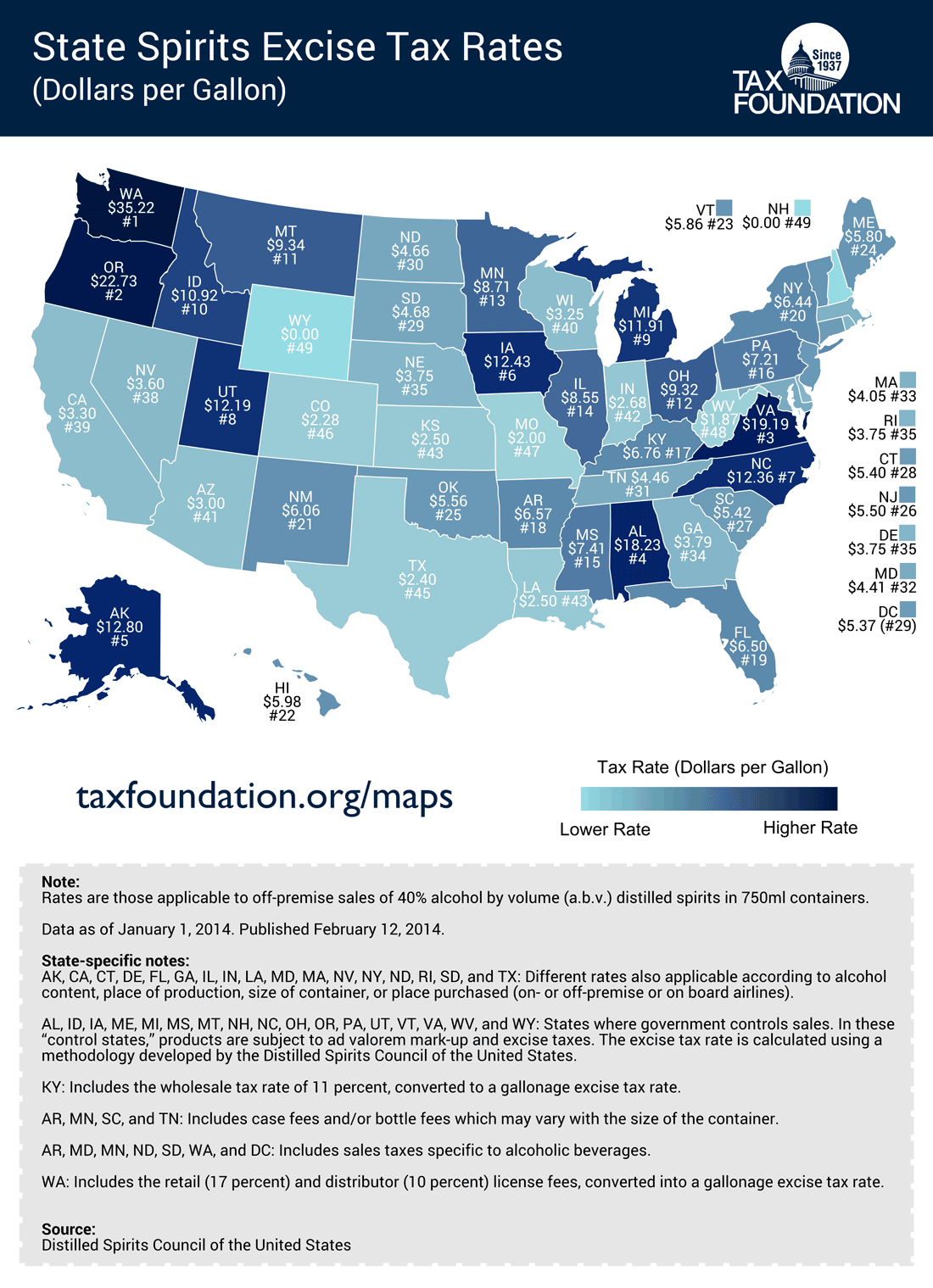

Across states, Washington levies the highest excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. rate on distilled spirits at $36.68 per gallon. The next highest rates are levied in Oregon, at $23.74 per gallon, and Virginia, at $23.47 per gallon. Spirits bear the lowest burden in Wyoming and New Hampshire, with both control states levying an effective rate of $0.00 per gallon, followed by Missouri at $2.00 per gallon.

The significant disparity in tax rates across states underscores the complex tax and regulatory environment governing distilled spirits. Distilled spirits are generally taxed according to increasingly hard-to-define categories of alcohol. The arcane categorical system could be made simpler and more neutral by modernizing the structure and taxing according to actual alcohol content. This would enable neutral tax treatment across different types of alcohol, incentivizing competition between spirits, beer, and wine.

As the product landscape continues to develop and calls for policy reform intensify, principled public policy changes should support both industry growth and responsible consumption with neutral, simple, and transparent taxes.

Distilled Spirits Taxes by State, 2026

State Spirits Excise Tax Rates in Dollars per Gallon, as of January 2026

| State | Spirits Tax Rate per Gallon | Rank |

|---|---|---|

| Alabama (a) | $22.87 | 4 |

| Alaska (b) | $12.80 | 10 |

| Arizona | $3.00 | 43 |

| Arkansas (c, d) | $9.76 | 14 |

| California (b) | $3.30 | 40 |

| Colorado | $2.28 | 47 |

| Connecticut (b) | $5.94 | 26 |

| Delaware (b) | $4.50 | 34 |

| Florida (b) | $6.50 | 22 |

| Georgia (b) | $3.79 | 37 |

| Hawaii | $5.98 | 25 |

| Idaho (a) | $12.94 | 9 |

| Illinois (b) | $8.55 | 20 |

| Indiana (b) | $2.68 | 44 |

| Iowa (a) | $15.14 | 7 |

| Kansas | $2.50 | 45 |

| Kentucky € | $9.56 | 15 |

| Louisiana (b) | $3.03 | 42 |

| Maine (a) | $11.93 | 12 |

| Maryland (b, d) | $5.46 | 29 |

| Massachusetts (b) | $4.05 | 36 |

| Michigan (a) | $14.61 | 8 |

| Minnesota (c, d) | $8.74 | 19 |

| Mississippi (a) | $9.38 | 16 |

| Missouri | $2.00 | 48 |

| Montana (a) | $10.55 | 13 |

| Nebraska | $3.75 | 38 |

| Nevada (b) | $3.60 | 39 |

| New Hampshire (a) | $0.00 | 49 |

| New Jersey | $5.50 | 28 |

| New Mexico | $6.06 | 24 |

| New York (b) | $6.44 | 23 |

| North Carolina (a) | $18.23 | 5 |

| North Dakota (b, d) | $4.93 | 32 |

| Ohio (a) | $12.33 | 11 |

| Oklahoma | $5.56 | 27 |

| Oregon (a) | $23.74 | 2 |

| Pennsylvania (a) | $7.48 | 21 |

| Rhode Island (b) | $5.40 | 31 |

| South Carolina (c) | $5.42 | 30 |

| South Dakota (b, d) | $4.93 | 32 |

| Tennessee (c) | $4.46 | 35 |

| Texas (b) | $2.40 | 46 |

| Utah (a) | $16.07 | 6 |

| Vermont (a) | $9.06 | 17 |

| Virginia (a) | $23.47 | 3 |

| Washington (d, f) | $36.68 | 1 |

| West Virginia (a) | $8.98 | 18 |

| Wisconsin | $3.25 | 41 |

| Wyoming (a) | $0.00 | 49 |

| DC | $6.68 | (22) |

(b) Different rates also applicable according to alcohol content, place of production, size of container, or place purchased (on- or off-premises or onboard airlines).

(c) Includes case fees and/or bottle fees which may vary with size of container.

(d) Includes sales taxes specific to alcoholic beverages.

(e) Includes the wholesale rate of 11%, converted to a gallonage excise tax rate.

(f) Includes the retail (17%) and distributor (5%/10%) license fees, converted into a gallonage excise tax rate.

Note: Rates are those applicable to off-premises sales of 40% alcohol by volume (ABV) distilled spirits in 750mL containers. At the federal level, spirits are subject to a tiered tax system. Federal rates are $2.70 per proof gallon on the first 100,000 gallons per calendar year, $13.34/proof gallon for more than 100,000 gallons but less than 22.23 million, and $13.50/proof gallon for more than 22.23 million gallons. DC's rank does not affect states' ranks, but the figure in parentheses indicates where it would rank if included.

Source: Distilled Spirits Council of the United States; Alcohol and Tobacco Tax and Trade Bureau.

Data compiled by Jacob Macumber-Rosin , Adam Hoffer

Distilled Spirits Taxes by State, 2025

State Spirits Excise Tax Rates (Dollars per Gallon) as of January 1, 2025

| State | Rate | Rank | Notes |

|---|---|---|---|

| Alabama | $22.87 | 3 | (a) |

| Alaska | $12.80 | 10 | (b) |

| Arizona | $3.00 | 44 | |

| Arkansas | $9.47 | 15 | (c, d) |

| California | $3.30 | 41 | (b) |

| Colorado | $2.28 | 48 | |

| Connecticut | $5.94 | 27 | (b) |

| Delaware | $4.50 | 35 | (b) |

| District of Columbia (DC) | $6.68 | 22 | (d) |

| Florida | $6.50 | 23 | (b) |

| Georgia | $3.79 | 38 | (b) |

| Hawaii | $5.98 | 26 | |

| Idaho | $12.94 | 9 | (a) |

| Illinois | $8.55 | 20 | (b) |

| Indiana | $2.68 | 45 | (b) |

| Iowa | $15.14 | 7 | (a) |

| Kansas | $2.50 | 46 | |

| Kentucky | $9.56 | 14 | (e) |

| Louisiana | $3.03 | 43 | (b) |

| Maine | $11.93 | 12 | (a) |

| Maryland | $5.46 | 30 | (b, d) |

| Massachusetts | $4.05 | 37 | (b) |

| Michigan | $14.61 | 8 | (a) |

| Minnesota | $8.74 | 19 | (c, d) |

| Mississippi | $8.88 | 18 | (a) |

| Missouri | $2.00 | 49 | |

| Montana | $10.55 | 13 | (a) |

| Nebraska | $3.75 | 39 | |

| Nevada | $3.60 | 40 | (b) |

| New Hampshire | -- | -- | (a) |

| New Jersey | $5.50 | 29 | |

| New Mexico | $6.06 | 25 | |

| New York | $6.44 | 24 | (b) |

| North Carolina | $18.23 | 5 | (a) |

| North Dakota | $4.93 | 33 | (b, d) |

| Ohio | $12.33 | 11 | (a) |

| Oklahoma | $5.56 | 28 | |

| Oregon | $22.86 | 4 | (a) |

| Pennsylvania | $7.48 | 21 | (a) |

| Rhode Island | $5.40 | 32 | (b) |

| South Carolina | $5.42 | 31 | (c) |

| South Dakota | $4.93 | 33 | (b, d) |

| Tennessee | $4.46 | 36 | (c) |

| Texas | $2.40 | 47 | (b) |

| Utah | $16.07 | 6 | (a) |

| Vermont | $9.06 | 16 | (a) |

| Virginia | $23.47 | 2 | (a) |

| Washington | $36.98 | 1 | (d, f) |

| West Virginia | $8.98 | 17 | (a) |

| Wisconsin | $3.25 | 42 | |

| Wyoming | -- | -- | (a) |

(b) Different rates also applicable according to alcohol content, place of production, size of container, or place purchased (on- or off-premise or onboard airlines).

(c) Includes case fees and/or bottle fees which may vary with size of container.

(d) Includes sales taxes specific to alcoholic beverages.

(e) Includes the wholesale tax rate of 11%, converted to a gallonage excise tax rate.

(f) Includes the retail (17%) and distributor (5%/10%) license fees, converted into a gallonage excise tax rate.

Note: Rates are those applicable to off-premise sales of 40% alcohol by volume (a.b.v.) distilled spirits in 750ml containers. At the federal level, spirits are subject to a tiered tax system. Federal rates are $2.70 per proof gallon on the first 100,000 gallons per calendar year, $13.34/proof gallon for more than 100,000 gallons but less than 22.23 million and $13.50/proof gallon for more than 22.23 million gallons. D.C.’s rank does not affect states’ ranks, but the figure in parentheses indicates where it would rank if included. The alcohol excise tax provisions of the Tax Cuts and Jobs Act were made permanent as of Dec. 27, 2020.

Source: Distilled Spirits Council of the United States; Alcohol and Tobacco Tax and Trade Bureau.

Data compiled by Adam Hoffer

Notable Changes from 2025

- The tax on spirits in Oregon increased by $0.88 per gallon, pushing the state from the 4th to 2nd highest tax rate in the country.

- The tax on spirits in Mississippi increased by $0.50 per gallon.

- The tax on spirits in Washington decreased by $0.30 per gallon, though the state remains the highest tax rate in the country by a significant margin.

- The tax on spirits in Arkansas increased by $0.29 per gallon.

Myriad tax policies are applied to distilled spirits across state jurisdictions. To allow for comparability between states, a standard measure across the various ways spirits are taxed and sold was developed. The governments of 17 states have granted themselves a monopoly over liquor sales. In these “control” states, the government can leverage its monopoly power to increase prices in lieu of levying a formal tax. The data reflect the implied excise rates in those states with government-controlled liquor stores.

Some control states, like Oregon and Virginia, use their market power to levy notably high tax rates compared to other jurisdictions. Almost all control states have effective excise tax rates on spirits higher than the median rate across the country. Wyoming and New Hampshire, however, have set prices low enough to effectively be selling spirits without levying an additional tax. Instead, these states generate revenue from alcohol sales themselves through government stores.

The data also include any additional fees and special sales taxes applied to spirits in addition to legislated excise taxes. These include case and bottle fees, special sales taxes applied to spirits sales, wholesale taxes, and retail and distributor license fees. Distilled spirits tax rates may also vary within states according to alcohol content, place of production, or place purchased (such as on- or off-premises or onboard airlines). For these estimates, sales are assumed to be off-premises sales of 40 percent alcohol spirits in 750 mL containers.

Distilled spirits bear an additional burden in every state from a federal excise tax. The first 100,000 proof gallons of distilled spirits manufactured in America per calendar year are taxed at a reduced rate of $2.70 per proof gallon, which would be $1.08 per gallon of 40 percent ABV spirits. The next 22.13 million proof gallons manufactured in America per calendar year are taxed at $13.34 per proof gallon ($5.34 per gallon of 40 percent ABV spirits). Any additional spirits manufactured in America and all spirits imported into the country are taxed at the general rate of $13.50 per proof gallon ($5.40 per gallon of 40 percent ABV spirits).

The total impact of the many federal, state, and local taxes and fees is significant. Most of the taxes are levied on producers, wholesalers, or retailers and baked into the final retail price rather than broken out separately on a bill or receipt like a sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. , so consumers may not be cognizant of just how much they are paying in taxes. The various taxes combine to account for about half of the price of a typical bottle of spirits.

Just as with cigarettes, significant differentials in tax burdens between nearby jurisdictions incentivize cross-border trade and smuggling. For instance, residents of Washington, the state with the highest spirits taxes, are estimated to account for 8 percent of purchases in Idaho, a neighboring control state with a lower effective tax burden (though still the 9th highest in the country). That 8 percent of purchases amounts to approximately $25.3 million in sales.

The recent tariffs and trade war have hit the spirits industry particularly hard, amid underlying consumer trends of young people opting for less alcohol. Policymakers should remain mindful of the unsuitability of excise taxes for raising general revenues. With steady ad quantum taxes losing real value to currency debasement and ad valorem taxes subject to significant fluctuations from behavioral changes or market dynamics, state governments that depend on spirits taxes for general spending may find themselves with unforeseen budget gaps.

A recent court ruling struck down an 1868 federal law criminalizing distilling alcohol at home, a ban ostensibly put in place to prevent evasion of the federal excise tax. This could shake up the industry further, but if the Supreme Court takes up the case, it is likely to be upheld under the Court’s extremely expansive interpretation of the Commerce Clause.

Distilled spirits exist within a complex taxation and regulatory landscape. Alcohol is generally taxed using a categorical system that treats beer, wine, and spirits differently, even after adjusting for alcohol content. Oregon, for instance, taxes one proof gallon of spirits more than 33 times as much as one proof gallon of beer. The rigid statutory categories also often face challenges adapting to innovation in the industry and treating new products properly, like with ready-to-drink cocktails.

Modernizing the arcane categorical system by instead taxing according to alcohol content would make the broader alcohol tax system simpler and more neutral. Understanding the tax framework is crucial for both consumers and policymakers as the industry and the policy evolve for the most popular type of alcohol in the country.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe